Daily Summary – January 21, 2021

Daily Summary – January 21, 2021

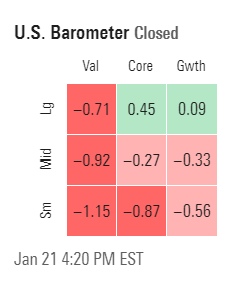

Day 2 of the Biden administration had some of the feel of Day 1, with value and small caps weak and large core and growth outperforming, but the overall tone was much less positive with much of the market declining, led to the downside by reopening stocks on the back of cont'd pessimistic talk from the White House about the near term amidst the backdrop of a European meeting to potentially lock down their continent for a period of time. In terms of indices, the result was NDX and Naz with nice gains of 0.82 and 0.55% respectively, but SPX basically flat, and RUT sold down nine tenths. The style box looked worse with just two green boxes and only one that was solidly in green territory (large core).

Technically this pushed RUT down towards the bottom of its channel. Also RUT RSI got another above to under 70 which is generally a bearish indicator but it's flipped around that a couple of times. SPX remains at the top of its channel while Naz and NDX have pushed up over the top (see NDX example below). Last time this happened (indices ran through the top of a weeks long channel) was end of August and almost immediately after it happened we got a quick 10% slice (see second chart). Not predicting anything, just noting.

Here's that prior period.

SPX sector flag deteriorated markedly with only three green sectors (same as y'days leaders - tech, discr, and comms) with tech only one up over 1%. All other sectors down at least three tenths with three (fins, materials, and energy) down over 1% led by energy which got sold down over 3%. Did hold support for now at least.

In key subsectors, semi's bounced back to continue their near parabolic run of the past couple of weeks, up another 1.5%. Retail also did well while transp (-1.65%) and small bios (XBI down over 2%) were both sold. Large bios (IBB) did a little better but still solidly red.

Breadth back to underperforming outside of Naz volume which was 69% positive. That has cont'd to hold up well, which is one difference between now back in August. But issues were v weak at only 43% positive, and NYSE was also v weak at 40% of positive volume and 38% of issues. That's the 3rd poor breadth day in the past 4 for NYSE. I'm raising a bit of caution but we've seen this pattern as recently as a week or so ago, so not buying any hedges or anything. Does increase the odds for cont'd weakness in the SPX and RUT though.

Outside of equities, not a lot of action today. Mild losses in crude, VIX, and long bonds, slightly bigger losses in nat gas and dollar with dollar pulling back to its 20-day MA, and mild gains in gold but remains under that resistance. Copper was flat.

Overnight and tomorrow we'll get global Markit PMI's and UK retail sales as well as existing home sales and EIA in the US. Lighter day for earnings with just 22 companies reporting and none over $50B market cap. And we'll continue to get information from the Biden Administration (as well as probably cont'd dire warnings out of Europe) which I have a feeling will continue to get a sell the news response for the time being.

Comments

Post a Comment