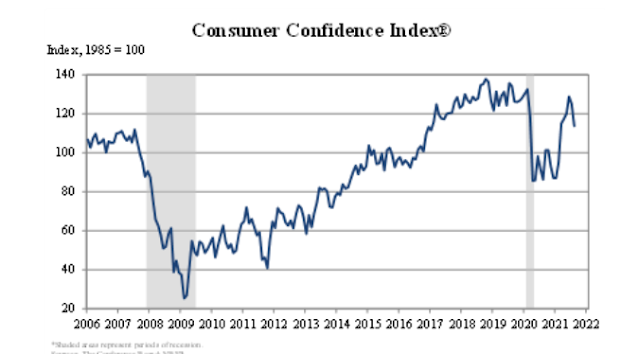

US CB Consumer Confidence Aug: 113.8 (est 123.0; prev 129.1) - August CB confidence report pulls back but not as much as UofM

US CB Consumer Confidence Aug: 113.8 (est 123.0; prev 129.1) After the "cratering" we saw in UofM the Conference Board consumer confidence index was also weak but stayed well above the pandemic lows. The headline fell by around 12 points to 113.8 with the present situation falling by 10 points to 147.3 and the expectations index falling by 12 points to 91.4. Cutoff date was August 25th. Same issues as UofM noted (Delta variant and inflation) were seen here. Positively, current labor market conditions remained very strong. From the report: The Conference Board Consumer Confidence Index® declined in August, following a decrease in July (a downward revision). The Index now stands at 113.8 (1985=100), down from 125.1 in July. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—fell to 147.3 from 157.2 last month. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market ...