Daily Summary – August 30, 2021 - A Mixed Bag

Daily Summary – August 30, 2021 - A Mixed Bag

Please excuse typos.

After Friday's broad move higher in which most all stocks participated to some degree, the market returned to the "either/or" which we had escaped the last few days but which otherwise has characterized most of the past 12 months. It's "either" those large growth names typified by the FAANG stocks doing well "or" everything else. Today it was the former which pushed the SPX (+0.43%), NDX (+1.12%) and Nasdaq (+0.9%) to new record highs while value stocks and small caps fell, with the RUT down a half percent. It's likely 10-year yields falling back to Tuesday's levels and crude coming off a bit were at least in part to blame for the cyclical weakness.

Style box favoring large caps and growth.

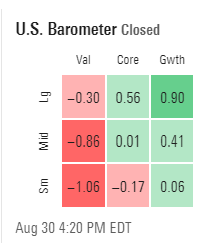

SPX Sector Flag

Weaker SPX sector flag which went from ten to seven green sectors with RE leading followed by those FAANG sectors. The four red sectors were our "core cyclicals" with energy and financials the only two down over -0.12% though.

Here's current expectations (no different than what we noted this morning):

As gasoline demand starts its normal seasonal decline (although typically Labor Day week is a big travel week, so I wouldn't be surprised to see a pop from that and those stocking up in front of Hurricne Ida).

Reported on pending home sales and Dallas Fed today. Links below.

US Pending Home Sales (M/M) Jul: -1.8% (est 0.4%; prev R -2.0%) - Pending home sales pull back in July as supply remains scarce - details

https://seekingalpha.com/instablog/15085872-cbus-neil/5633604-us-pending-home-sales-m-m-jul-minus-1_8-percent-est-0_4-percent-prev-r-minus-2_0-percent

Dallas Fed Manufacturing Survey: +9 vs. +25 consensus and +27.3 prior - Dallas Fed Mfg comes in well below expectations as supply chains and prices constrain new orders and shipments

https://seekingalpha.com/instablog/15085872-cbus-neil/5633689-dallas-fed-manufacturing-survey-plus-9-vs-plus-25-consensus-and-plus-27_3-prior-dallas-fed

Next 24

[B}anks are so flush with liquidity, they are now giving the ECB cash as collateral for the loans they receive. Yes, you read that correctly. Banks have borrowed money from the ECB -- and given the ECB the money back as collateral for the loan.

We can see this in data provided by the weekly financial statement, which has a line item called "deposits related to margin calls." In any other time, an increase in this line item would be a sign of severe stress, as it would mean the collateral banks had posted with the ECB to secure their lending had fallen so much in value, the ECB has made a margin call -- think Greek sovereign bonds circa 2011.

What the current rise is pointing to, though, is banks having nothing else to do with the cash, and by using it as security for the loan they get a handy interest rate income on the difference between the deposit rate of minus 0.5% and a TLTRO rate of potentially minus 1%. It also means that banks -- by giving the cash straight back to the ECB without doing anything else with it -- are effectively sterilizing a proportion of total liquidity the central bank provides.

Monthly balance sheet data shows that the Bundesbank accounts for all of this "margin call" cash. It will be worth watching to see if this number disappears at the end of September when banks are allowed to start making early repayments on the cash they borrowed under TLTROs in 2019 and 2020.

Comments

Post a Comment