Daily Summary – March 31, 2021 - Into April We Go

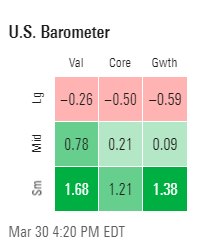

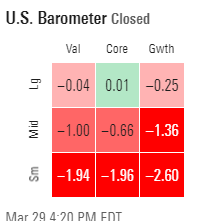

Daily Summary – March 31, 2021 - Into April We Go I ended yesterday's summary insinuating we'd see downside today due to what I thought would be some lingering quarter-end rebalancing, and while we did seem to get some of the latter (rebalance) it wasn't out of equities and into bonds as I thought might happen after one of the worst quarters for bonds ever, but rather between equity sectors as some of the first quarter's laggards (tech, discr, utes, comms, and health care) finished green while the stronger sectors (basically the rest) finished red led to the downside by the two biggest winners, energy and financials. We also saw it within sectors as for example high flying GME and AMC (up 908 and 283% respectively) finished red, while AAPL and AMZN which both finished down for the quarter finished green. The same was true of indices with NDX and Naz (which finished the quarter with very moderate gains) finishing the day up around 1.5% (which was over half of the ove...