Daily Summary – March 29, 2021 - Another Risk Off Day

Daily Summary – March 29, 2021 - Another Risk Off Day

I ended Friday's summary with

"So, overall, I'm encouraged by the broad based rally today, but I still see headwinds in technicals, breadth, and sentiment. So my inclination is to look for weakness early in the week that we rally from...."

What I didn't take into account is the breadth of the losses related to the Archegos family fund blowup which caused a bit of a risk off mood as did the director of the CDCs warning of "impending doom". Nevertheless, bonds did not benefit with the 10-year yield pushing back up above the 1.7% level towards its recovery highs which dinged growth stocks a bit. Value stocks on the other hand were hurt by financials due to potential after-shocks from the Archegos issue (as well as what seems to be still profit taking in 1Q winners as most of those sectors were weak).

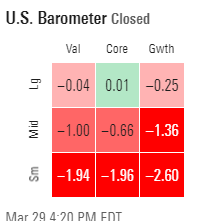

The result was a very mild down day for the big cap dominated SPX and NDX, a little bigger losses in the Naz while the RUT got whacked for almost 3%. If it feels like it's really come off the boil, it has. According to Bespoke, stocks in the Russell 2000 are down an average of 22.3% from their 52-week highs, and nearly 200 are down over 50%. Compare that with the S&P 500 where the average decline from their 52-week highs is just over 8% and Viacom is the only stock down 50% from its 52-week high.

As those index results might indicate, the style box was deeply red at the bottom, less so towards the top (and large core finished just in the green). Slight bias to value over growth.

Technically nothing really new to report from what I'm looking at. SPX remains in good shape with a lot of issues with the other three.

Fund managers sold petroleum last week at the fastest rate since successful coronavirus vaccines were announced in November, as a resurgence of infections and a loss of upward price momentum triggered profit-taking.Hedge funds and other money managers sold the equivalent of 88 million barrels of petroleum futures and options in the week to March 23, the fastest rate of selling since Nov. 3, according to exchange and regulatory data.The heaviest selling was concentrated in Brent (-51 million barrels) but there were also sales in NYMEX and ICE WTI (-21 million), U.S. gasoline (-4 million), U.S. diesel (-5 million) and European gasoil (-8 million).Most of the sales were driven by the liquidation of existing bullish long positions (which were reduced by 73 million barrels) rather than the creation of new bearish short ones (just 16 million barrels of shorts were added).

Prior to the sell-off, portfolio managers' positions had become lopsided, with a net position of 913 million barrels, which was in the 83rd percentile for all weeks since 2013.

But the hedge fund community is still very bullish towards oil, with a net position of 824 million barrels (76th percentile) and long/short ratio of 4.75 (66th percentile), just slightly more cautious than a few weeks ago.

Comments

Post a Comment