Daily Summary – March 30, 2021 - Into Month End We Go

I ended yesterday's summary with

"Given today's action, I'm inclined to look for more downside tomorrow, especially given the buying volume. I still think we rally within the first few trading days of April, but I don't think we're ready to quite yet."

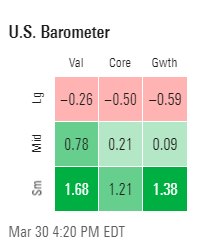

That was true of the SPX and and Naz which were weighed down by weakness in large caps, but small caps found their footing today following the largest beat in consumer confidence since 2000 (which was the highest reading in a year although only about halfway back to pre-pandemic highs) and a bounceback in financials with the RUT powering up 1.72% to easily outpace the larger cap indices. SPX finished down a third of a percent while NDX weighed down by increasing 10-year yields fell little more than half a percent. Naz finished down around a tenth. The style box the opposite of yesterday's with green towards the bottom although still a bit of a value bias again today.

Technically nothing really new to report. SPX remains in best shape but a lot of issues with the other three. Despite the big rally RUT just joined the other two on the underside of that downtrend line that's capped things since 3/15.

SPX sector flag deteriorated a bit further today with only three sectors green and none up over 1% (there were three yesterday). Financials led to the upside bouncing back from yesterday's selloff followed closely by discr. Only one sector down over 1% (staples which reversed y'days strong gain) although four others were down at least three quarters of a percent.

On major sector charts, not a lot new. Industrials hit an ATH and got a go long crossover on daily MACD but has an RSI divergence.

In major subsectors, transp, homebuilders and retail were all strong all up over 1% with the former setting an ATH. Bios bounced back a bit today to finish mildly green while semi's finished mildly red.

Breadth surprised to the upside with 66 and 67% of volume positive on NYSE and Naz respectively. Issues not quite as strong but up 61 and 58% respectively. Those are pretty good numbers particularly for Naz which finished red (NYSE was benefited by the strong gains in small caps).

Outside of equities, as noted above 10-yr yield did edge up a basis point today but that was off the highs that were 5 bp's higher. This supported the dollar which continued to push up over that 200-DMA, which in turn pressured commodities with crude, gold, copper, and nat gas also closing down at least 1%. In terms of oil, the OPEC+ technical committee met today setting the stage for the policy meeting tomorrow. No big news but demand was revised down due to the European third waive and the group made a number of cautious notes, but they nevertheless revised up their estimates for 2021 inventory drawdowns. Expectations are for a rollover of the existing level of production at least one more month (i.e., keeping current cuts).

Interestingly also red today despite the general market weakness was the VIX which fell right back under 20 but remains above the pandemic lows a point lower.

Overnight we'll get final March Chinese PMI's and a bunch of data from Europe including German employment and EU CPI followed by mortgage apps, ADP, pending home sales, and EIA here in the US. We'll also get those results of the OPEC+ meeting, and we do get MU and WBA earnings (thought WBA would be bigger than $45B market cap).

It's also the last trading day of the month, so will be interesting to see if we have any more rebalance (or anti-rebalance as Marko Kolanovic called for). While it seems like we had some rebalancing action (buying of bonds selling of 1Q winners) earlier in the month, haven't really seen that action since then (at least in terms of buying bonds, I guess stocks have been relatively weak particularly small caps). I'm encouraged by the tickup in up volume today but it's only one day. But one thing to note is overall breadth remains in very solid shape as indicated by stocks over their 200-DMAs.

And sentiment seems like it is maybe growing a bit more cautious.

But overall I dislike the current levels of bullish sentiment in most of the surveys as well as the technicals, so I'm not ready to call for a rally just yet, particularly in front of what I think will be some more rebalancing action out of stocks.

Misc

I'm having trouble keeping up with things during the day, so I thought I'd start to post miscellaneous interesting things I came across during the day at the end here. One was on the power of retail traders.

For anyone thinking that retail is overblown because they represent such a small portion of overall market cap, a study indicates not to dismiss their potential impact.

Also Barron's ran an article stating that they were seeing a potentially more difficult approval process from the FDA.

Which was followed today by this.

|

WSJ - FTC Challenges Illumina’s Planned Acquisition of Liquid-Biopsy

Firm Grail

|

|

|

|

The FTC sued to block

Illumina’s $7.1 billion deal for Grail, a major test in challenging a

vertical merger in which companies don’t compete directly. | |

Hmm.

But in a spot of good news.

To see more content, including summaries of some of today's economic reports go to

https://sethiassociates.blogspot.com

Comments

Post a Comment