Daily Summary – January 22, 2021

Daily Summary – January 22, 2021

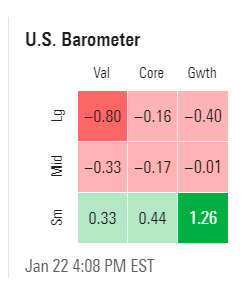

Day 3 of the Biden Era started out with a similar theme to Days 1 and 2 with large caps and growth outperforming but with a more negative tone than the first two days, with all major indices opening solidly in the red. But right at 9.45 am when the better than expected Markit ISM's were released (actually right before hmm) indices turned around and started heading up until a little after 10 am when all the indices pulled back. From there, paths diverged a bit. The small caps, which had steadily traded lower since the inauguration, bottomed well off the lows and moved higher in a seesaw pattern until 2.15 pm when they took off, ramping right up into the close with the RUT finishing up 1.28%. Naz also trended up, although not quite as smoothly to finish modestly green (up one tenth) due to a last minute drop of several tenths (not sure of the catalyst). SPX, and NDX on the other hand retested the lows, and while they at one point got to around breakeven levels, they also sold off just before the close to finish solidly red down three tenths. Style box clearly shows the bias to small caps and growth, making that small growth box the easy winner today. For the week, Naz was the winner up 4.2%, NDX up 3.4% while the SPX and RUT were around 2%.

And, of course, we'll continue to get more stuff from the new administration. Whether you agree with their politics, he's staffed is organization with a lot of pros, and they seem to know how to get things done. But I'd love to see a little more optimism. I don't think all of the talk about "dark winters" and "the worst is yet to come" is helping.

Finally, one other thing I wanted to note is something I should have thought to look at last week, which is what happened last earnings season. I'm sure most will remember that stocks in general did not react as typical to earnings beats (don't have the precise numbers but the reaction was far less positive to beats than was typical). What I at least had forgotten was that starting on the day of the JPM earnings (10/13) the indices sold off for the most part for a couple of weeks (bottoming on 10/30 which marked the end of our last major selloff). During that time SPX sold off -9.2% (see chart), NDX -10.7% RUT -7.5%, and Naz -9.6% despite one of the highest beat rates for earnings and revenues in history. I have no idea if that translates to this go 'round, just thought it was interesting, as we seem to have a similar dynamic going on (companies with earnings beats on net are finishing red). We'll see. Regardless, have a great weekend!

Comments

Post a Comment