Daily Summary – January 25, 2021

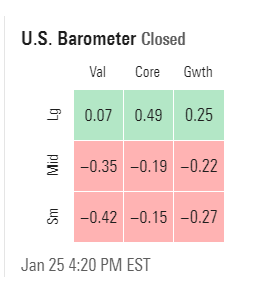

I mentioned last Friday that post-JPM earnings last quarter, the markets sold off pretty substantially. As today progressed, it looked like we might follow that pattern this go round, as markets sold off sharply at 10.45 am going from mild gains to solid losses before bottoming just as sharply 20 minutes later and climbing throughout the day into the close. While there were lots of individual movers (anything with heavy short interest was a buying target today it seemed) the general bias to the FAANG type names from last week carried over into today with the NDX (which led last week) leading again today up 0.87%. Naz was up seven tenths, SPX 0.36% and the RUT lagged finishing down a quarter percent. Style box was consistent with small value again the biggest loser and large core the best.

Technically while some channel lines were broken intraday, by the end everyone was back where they started with Naz and NDX above their channels of Nov-last week, RUT and SPX in the middle. All look ok except RUT is really starting to look tired as the RSI has now printed a series of lower highs while price has gone slightly higher since 1/14:

Price

SPX sector flag a bit improved with 7 green sectors led by utes, only sector up over 1%, and which has steadily climbed higher since intra-day bottom on 1/12. Energy led the losers today, only sector down over 1% (although it recovered about half its losses during the day).

In key subsectors, semi's continued to consolidate, recovering from solid losses to finish mildly green as did transp (although transp didn't quite make it to green). Bios flew with XBI up over 3%, and retail outperformed, but the XRT finish of up 1.75% misses the story, as it was up over 6% at one point today on the back of huge moves from heavily shorted stocks like GME, BBY, etc.

Breadth back to disappointing today with only 59% of volume and 40% of issues positive NYSE, 59 and 46% Naz. The fact that over half the issues were red is not great, and neither is the fact that breadth was around the same levels (a little better on Naz in fact) on Friday where SPX was red and Naz was barely green.

Outside of equities, VIX at one point pushed all the way up to the 26 level before pulling back to finish around 23 and back under its 50-day. Nat gas had a big day up over 6% and pushing to the underside of MA resistance. Crude also recovered from losses to finish green, as did long bonds, copper and dollar (very mildly). 10-yr yield did push down to its 20-day MA. Gold finished basically flat.

Overnight we'll get UK unempl followed by Redbook, home prices, CB consumer conf, Richmond PMIs, and API in the US. Big day for earnings with 88 co's and 21 $50B or larger led by MSFT. So between data and earnings, will be plenty to chew on during the day, especially when you add in cont'ing stories out of Washington. But the good news is that earnings continue to come in solid, and even better the latest Covid spike appears to be moderating globally, both of which should help to keep spirits up. We also should be getting data from JNJ anytime now. They do report earnings tomorrow. Hmm.

Comments

Post a Comment