Daily Summary – May 28, 2021 - A Tame Finish

Markets finished a relatively tame week with an appropriate finish with SPX, NDX, Naz, and RUT all finishing within a third of a percent of unchanged with all ending green other than RUT which was down two tenths. Gains were a little better earlier in the day but a chunk of selling just before the close knocked them down a bit. Interestingly, according to Helene Meisler of Top Charts, Naz has not had consecutive up/down days for two weeks.

For the week, all finished with gains, while for the month, SPX and RUT registered very mild gains while Naz and NDX were down less than 2%.

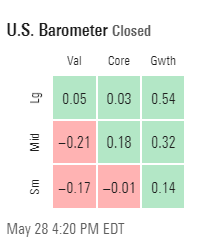

After taking a few days off, large growth back in the lead today. Some of that might have been some month-end rebalancing out of May winners into losers though. Next week will be interesting to see which reasserts leadership (or heaven forbid they both go up or down together).

And it was a great week for travel stocks.

Reminder markets closed on Monday to commemorate Memorial Day.

Major Market TechnicalsOnce again no changes on the technicals, but in case I didn't note it yesterday, SPX did get a MACD go long trigger. It's RSI also broke over its downtrend line, so that bodes well for further gains there. So now all four of the indices I track have bullish MACD and RSI configurations. All are also above all of the key moving averages I track. RUT did end up failing at that 2285 level we identified yesterday. So that sets up as resistance for next week.

And according to Bespoke all the major US indexes are above their 50-DMAs.

SPX Sector Flag

More green sectors in the SPX sector flag today with seven green (six yesterday), but none up over 1% (actually none up more than two thirds of a percent) (two over 1% yesterday) with defensives moving to the front from the back. Cyclicals took the top three spots today. No sector down more than half percent though. So very tight trading today.

SPX Sector Technicals

With such muted action for the day took a look at the monthly charts and all sectors look to be in good shape. Biggest issue is a couple are very overbought - materials, comm's and RE in particular.

Subsectors

Retail, homebuilders, and bios were red, semi's and transp green. Only sector to move more than 1% was retail down 1.26% (XRT).

Breadth

Breadth poor today for NYSE with only 43% of volume positive although 57% of issues. Naz better with 62% of volume positive but 50% of issues. Last day of the month and ahead of a holiday week, so not going to read anything into this today.

Commodities/Currencies/Bonds

Bonds - Despite the biggest increase in history for the Fed's preferred inflation measure (I know, I know base effects), and the numerous mentions of inflation in UofM survey (discussed below) as well as the Costco conference call today (CFO said "inflationary factors abound"), and after two green days which pushed the 10-yr yield up to its 50-DMA, yields nevertheless pulled back a bit today, falling a few basis points. This sets up that 50-DMA as more solid resistance going forward. Guess we can say that short-term inflation is priced in.

Dollar - It gave it a go in the morning, but basically reversed all of the daily gain to close barely green, right on that trendline it had broken through in the morning.

VIX - Stable at 16.76.

Crude - Wasn't able to sustain its gains falling a touch, but did close at the highest monthly close since 2018. It also appears to have conclusively broken over that trendline dating back to 2008, with a breakout on the monthly RSI, as well as getting very close to a monthly MACD go long signal.

And not surprisingly (based on the above), traders added a good amount to net length in week through May 25th.

But interestingly they reduced positions in Brent.

As consultancy Rystad becomes the latest to say more oil drilling will be needed in the future.

It also says that this can be consistent with climate goals.

Even if oil demand remains at 36 million bpd in 2050, it should be possible to reach the target of limiting the temperature rise to 1.5 degrees Celsius compared to pre-industrial times, it added.

Rystad’s analysis is likely to be welcomed by oil companies and oil producing countries, such as Norway, which have questioned the IEA’s analysis as it undermines the case for the industry to carry on producing oil in the medium term.

And just a reminder that OPEC+ meetings will continue with a decision expected on Tuesday. No changes to scheduled production increase are expected as they wait to see what happens in Vienna (Iran sanctions talks).

The OPEC+ deliberations will begin May 31 with a meeting of the delegate-level Joint Technical Committee to review supply-demand forecasts and assess member country compliance with quotas, which Platts calculated at 111% for April.

A nine-country Joint Ministerial Monitoring Committee co-chaired by Saudi Arabia and Russia is then scheduled to convene June 1, followed by the full OPEC+ meeting as soon as that ends.

Nat Gas - Solidly green today back over $3.

Gold - After starting red, reversed to green today for highest close since early January.

Copper - Tested top of its 20-DMA and bounced off to finish mildly green.

U.S. Data

Did report on personal income and spending/PCE today.

US Personal Income Apr: -13.1% (est -14.2%; prevR 20.9%; prev 21.1%); US Personal Spending Apr: 0.5% (est 0.5%; prevR 4.7%; prev 4.2%) - details and analysis

https://sethiassociates.blogspot.com/2021/05/us-personal-income-apr-131-est-142.html

UofM final May consumer sentiment also out today which saw expectations move up a bit but current conditions back a bit. Long term inflation expectations also fell a touch while 1-year remained in record territory.

US Univ. Of Michigan Sentiment Mar F: 82.9 (est 83.0; prev 82.8)

- Current Conditions: 89.4 (prev 90.8)

- Expectations: 78.8 (prev 77.6)

- 1-Year Inflation: 4.6% (prev 4.6%)

- 5-10 Year Inflation: 3.0% (prev 3.1%)

To put today's report into the larger historical context since its beginning in 1978, consumer sentiment is 3.8 percent below the average reading (arithmetic mean) and 2.7 percent below the geometric mean. The current index level is at the 37th percentile of the 521 monthly data points in this series.

Surveys of Consumers chief economist, Richard Curtin, made the following comments (bold is mine):

Consumer confidence remained largely unchanged at the reduced level recorded at mid-month. It is hardly surprising that the resurgent strength of the economy produced more immediate gains in demand than supply, causing consumers to expect a surge in inflation. Record proportions of consumers reported higher prices across a wide range of discretionary purchases, including homes, vehicles, and household durables - the average change in May vastly exceeds all prior monthly changes (see the chart). The impact of higher prices on discretionary spending will be offset by the more than $2 trillion increase in savings in the past year as well as by improving job prospects - an all-time peak proportion of consumers anticipated declines in the national unemployment rate during the year ahead. While higher inflation will diminish real incomes, the gains in spending will nonetheless be substantial. The key issue is whether the timing of spending decisions will advance due to the expected price increases. At present the growth in inflationary psychology is unlikely, but it cannot be completely dismissed. Early preventative actions are much less costly, but these actions are much more difficult when policy objectives include avoiding uneven distributional impacts across population subgroups. It will require keeping the level of stimulus higher for a longer period than would have seemed prudent in the past. The primary risk of this strategy is an accelerating inflation rate, which also has uneven distributional impacts. Shifting policy language and a small rate increase could douse inflationary psychology; it would be no surprise to consumers, as two-thirds already expect higher interest rates in the year ahead.

In terms of inflation, the topic de jure, there was of course plenty to chew on. “References to high home prices in evaluations of home buying conditions were made by 52% of all consumers, the highest proportion ever recorded; references to high vehicle prices were made by 26%, the highest since 1983, and mentions of high prices for household durables by 23%, the highest since 1982,” the survey noted, and Richard Curtin, the survey’s chief economist, flagged “record proportions of consumers” reporting higher prices for all manner of discretionary purchases, “including homes, vehicles, and household durables.”

Also released today was April advanced report on trade balance and inventories.

Trade deficit fell by 7.3% as exports were up by $1.7B (1.2%) while imports fell by $5.1B (2.2%). Wholesale inventories were up by 0.8% with both durable and non-durable inventories up while retail inventories fell by 1.6% due to a 6.3% decline in motor vehicles.

Going into a little more detail on the trade numbers exports would have been better if it wasn't for an 8% drop in autos. All other export categories were up led by capital goods up 4.8%. Imports fell in all categories by 1.8% or more except for capital goods which were up 0.2% and food and beverages which were up 3.4%. Full table below.

Next Week

Next week is normal for first couple of days but heavier Thursday and Friday culminating in the jobs report (also get factory orders on Friday).

ZM is largest US company reporting on Tuesday (none over $100B (although it's close)).

Overall

I'll have some info out at some point before open on Tuesday about June seasonality but it's generally not a great month. That said, technicals are in good shape, sentiment is not frothy, so I'll continue to look for higher prices for now.

Misc

Some other random stuff.

No surprises in the Biden "wish list" (which is what a Presidential budget really is, since it's Congress that writes and passes budgets).

And possible vaccine passports for the US?

And I mentioned AMC was 12% of the volume in the exchange yesterday (today was 10%). Here's another crazy stat (from today).

As Sony looking to address labor issues with robots. I'm sure we'll see more of this in places with similar demographic situations.

As do teens across the US.

Have a great Memorial Day weekend. If you're in the U.S., take a moment to remember those who gave the ultimate sacrifice so we could enjoy it.

To see more content, including summaries of some of today's economic reports and my morning and nightly updates go to https://sethiassociates.blogspot.com

Comments

Post a Comment