Memorial Day Update - 5/31/21

Memorial Day Update - 5/31/21

Thought I would give an update on some things I came across this weekend, and summarize where markets that were open today finished. US equity futures traded down today (they had a shortened session, closing at 1 pm) led by small caps with the RUT down almost half percent, NDX and SPX around a quarter percent. I'd caution reading too much into that as to trading for the upcoming week, though, as holiday volume is very thin (only 103k contracts traded on the SPX e-mini futures today (/ES) compared with 10x that on Friday).

Asia

In data, final read of China manufacturing PMI for May pulled back a touch. This had led to articles on China's recovery "peaking" (including the one below from China state media which is interesting).

China Manufacturing PMI May 51.0 (est 51.1; prev 51.1)

Also, I indicated last week that I thought it seemed like China was starting to push back on the yuan's rise, and that activity increased today with a hiking of the reserve ratio for foreign currency holdings (making it slightly more expensive for Chinese institutions to hold non-yuan assets). It also fixed the yuan starting point weaker in a further signal of its intentions. From Heisenberg Report:

On the heels of a virtually uninterrupted rally, the PBoC on Monday hiked the reserve ratio for banks’ foreign currency holdings. Starting in two weeks, financial institutions must hold 7% of their foreign exchange in reserve “in order to strengthen the management of foreign exchange liquidity,” a terse statement said.

It was the first move of its kind since 2007. The decision to make dollars and other FX more scarce onshore came as the yuan strengthened some 13% in just 12 months, taking the currency to levels last seen prior to Donald Trump’s trade war.

Beijing despises a one-way bet or, perhaps more aptly, the perception among market participants that the currency is a one-way bet.

The fix was weaker than forecast Monday following comments from a former central bank official who branded the yuan “overbought.” The PBoC’s Financial News ran a commentary arguing that a Fed taper, the strength of the US economic recovery, an abatement of the pandemic globally and, amusingly, the potential bursting of asset bubbles in the US, could catalyze yuan depreciation.

The market was unimpressed. The yuan barely reacted to the latest round of verbal intervention. In and of itself, it doesn’t seem particularly likely that increasing the reserve ratio for foreign exchange holdings will be sufficient to arrest the rally. Rather, it’s a warning shot meant to remind market participants that Beijing can do quite a bit more than talk.

Standard Chartered’s head of China macro strategy, Becky Liu, told Bloomberg that Monday’s move likely wasn’t “a one-off change, but [rather] the start of a trend.” Obviously, Beijing could lean more heavily into the daily fixings or simply intervene directly. If you’ve followed the PBoC’s currency management efforts over the past half-decade, you know the toolbox is virtually bottomless.

Japan had a lot of data out. April retail sales missed badly, industrial production missed but not as much and improved m/m (retail sales fell m/m), May consumer confidence pulled back a touch from April but beat expectations, and April housing starts beat as well.

Japanese Retail Sales (Y/Y) Apr 12.0% (est 15.2%; prev 5.2%); Japanese Retail Sales (M/M) Apr -4.5% (est -1.7%; prev 1.2%); Japanese Industrial Production (M/M) Apr P 2.5% (est 3.9%; prev 1.7%); Japanese Industrial Production (Y/Y) Apr P 15.4% (est 16.9%; prev 3.4%); Japan Consumer Confidence Index May 34.1 (est 33.0; prev 34.7); Japan Housing Starts (Y/Y ) Apr 7.1% (est 4.5%; prev 1.5%)

Europe

As with the US, European stocks broadly closed lower (UK was closed I believe). Didn't see any data of note.

Commodities/Currencies/Bonds

Bonds - No trading on US bonds today (bond market knows how to actually commemorate a holiday). Yields in Europe were little changed also.

Dollar - Fell 0.2% while euro, pound, and yen all rose.

VIX - Mildly red at 16.57.

Crude - Traded positively today pushing up to a 67 handle (WTI).

As I mentioned on Friday, big story today/tomorrow is the OPEC+ meeting going on. This is pulled from a Bloomberg article:

For oil traders, the biggest question in the market is how fast OPEC and its allies will revive production later this year. Next week they may get some clues.

When it meets on Tuesday, delegates said the alliance led by Saudi Arabia and Russia looks set to rubber-stamp output increases scheduled for the next two months.But more importantly, Riyadh and Moscow may offer insights on the next stage of their strategy: bringing back the millions of barrels a day that remain offline after being shuttered when the coronavirus struck.

In theory, there’s a yawning supply gap for the Organization of Petroleum Exporting Countries and its partners to fill in the second half of the year as economies open up and fuel demand soars. Yet the group will need to weigh that against the risk from renewed virus outbreaks in India and elsewhere, and the prospect of extra supply from fellow member Iran.

Once the current ramp-up is completed in July, OPEC+ nations will still have lots of spare production capacity, taken offline when demand crashed last year. On paper, this amounts to almost 6 million barrels a day, or roughly 6% of global supplies.Under a road map drawn up a year ago, OPEC+ is formally committed to withholding that output until April 2022. Yet that agreement was hastily struck at the height of last year’s tumult, and as customers start asking for extra barrels it will be tested.

For guidance on whether the cartel will allow some flexibility in its current plan, traders will look out for comments next week from Saudi Energy Minister Prince Abdulaziz bin Salman and his Russian counterpart. No decision on changes to policy beyond July is expected at this gathering, but any hints the ministers give will be closely scrutinized.

Tehran is engaged in nuclear negotiations with Washington that could lift U.S. sanctions on its crude exports. With an agreement, analysts expect the Islamic Republic could boost exports by 1.5 million barrels a day before the end of the year, limiting the need for extra barrels from other OPEC+ nations.

To safeguard against this, the Saudis will probably ask fellow members to ratify a pause until there’s more clarity on Iran, according to consultant Energy Aspects Ltd. Pressing for too long a wait, however, could aggravate old fault lines in the leadership of the coalition.

Riyadh and Moscow have often diverged on how quickly to bolster output, with the kingdom typically advocating restraint and Russia more impatient to expand sales volumes. The United Arab Emirates, another key player, has also shown eagerness to resume exports.

Whether Tehran’s comeback becomes a challenge for the group will depend on the strength of the demand recovery, according to Helima Croft, chief commodities strategist at RBC Capital Markets. As long as consumption remains robust, there’s unlikely to be much discord.

“However, if the market outlook darkens, then we would expect a much more contentious conversation,” Croft said.

“We see a shift from stigmatization toward criminalization of investing in higher oil production,” said Bob McNally, president of consultant Rapidan Energy Group and a former White House official.

As non-OPEC+ production increases less than global oil demand, the cartel will be in control of the market, executives and traders said. It’s a major break with the past, when oil companies responded to higher prices by rushing to invest again, boosting non-OPEC output and leaving the ministers led by Saudi Arabia’s Abdulaziz bin Salman with a much more difficult balancing act.

But it also noted that it had despite several attempts not received information on its findings of undeclared nuclear material.

Gold - Also up today getting over that 1900 level. Seems to me to have pretty clear sailing to the 1950 level. At some point though a pullback and test of support will be necessary to confirm the bull run.

Seasonally the solid May (gold was up over 10%) was an anomoly compared with past 10 years, but that seasonality predicts further solid gains in June and July.

Copper - Traded down a touch remaining above its 20-DMA.

Misc.

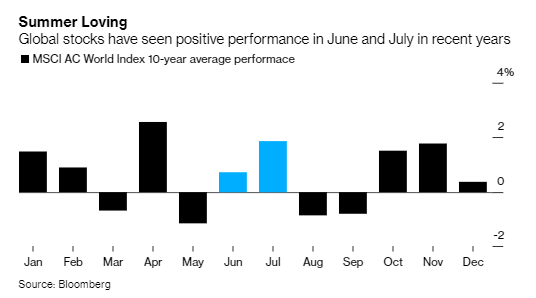

Said I'd talk about June seasonality. As I mentioned on Friday, not generally a great month. This is one of my favorite charts as it slices time periods in a variety of ways.

I like to look at more recent data so since 1988 it's generally been mildly down. This is also what you see in post election years. Those after a Presidential loss are even bigger, but remember these are very small sample sizes when you start to break it down this far. Suffice to say that June is not normally the greatest month for US stocks, particularly the last 20 years (although it should be noted we had a very solid over 6% gain last June (and it's been up at least marginally for the last six years) so you can only take these things so far). The good news is July is generally very solid. Here's another less granular table from Bespoke focusing on the Dow.

And bond spreads (this time IG) continue to hit new post-GFC tights.

As foreign buyers significantly have stepped up purchases of US debt at least through March (but believe this had continued as we've noted increasing indirect buying in recent Treasury auctions).

And I mentioned on my report on personal income that wages had increased and personal income in total remained far above pre-pandemic levels, but what I didn't realize is that personal income less transfer payments (so personal income taking government assistance out) had recovered all of its pandemic decline.

Also on Friday gave some detail on the UofM survey that saw inflation expectations at record highs, but an interesting analysis from the WSJ shows that this is due to an outsized move from a cohort that expects a huge jump. The top 25% in responses sees over 4.5% inflation during the next 5-10 years while the median remains just above 2.5% (which is well below the average of 3.4%). Apparently multiple respondents saw inflation of 10% or more per year.

But they see upside risk as well as likely wage inflation that will push CPI up near the 5-year breakeven level of 2.7%.

The closing of the output gap (when gross domestic product equals its potential) means that the recessionary slack in the economy will be gone for the first time since before the Great Recession. Via the traditional Phillips curve relationship, this should mean higher inflation. However, the experience of the past decade has suggested that the Phillips curve may have flattened somewhat, meaning less sensitivity of inflation to the output gap.

More concretely, we expect that very tight labor markets over the next few years will lead to high wage growth, which should create widespread inflation pressures. We project the unemployment rate to dip to an extraordinarily low 3% over 2022-24. These very tight labor markets will be necessary to pull formerly discouraged and marginal workers into the labor market, pushing labor force participation up to its potential. To be clear, this is just a one-time source of inflationary pressure, as once the marginal workers are in the labor market, their presence should be sticky. But it will be a prolonged process over the next several years.

Additionally, we think inflation risks are weighted to the upside, given the Fed’s willingness to let inflation run above its 2% long-run target for a while to make up for the fact it was below its 2% target for much of the 2010s.

Altogether, this means we forecast PCE (total and core) inflation averaging about 2.3% over the next five years. Given that the CPI usually runs about 30 basis points higher than the PCE, this implies 2.6% CPI inflation. This is fairly close to the 2.7% five-year break-even rate implied by Treasury Inflation-Protected Securities, which use the CPI.

And one more on inflation (or breakevens in this case - the difference between "normal" Treasury yields and TIPS (inflation protected)). Breakevens are often seen as a market priced determination of future inflation expectations. But Deutsche Bank for one thinks Fed purchases in this relatively thin market (as compared to "normal" Treasuries) are skewing the results. They note the strong correlation between Fed buying and the inflation risk premium.

This was echoed by a Bloomberg article recently - “If you’re buying every risky asset in sight because you think Treasurys are screaming that inflation is finally coming back, beware,” Bloomberg’s Edward Bolingbroke said. “You might be acting on a false signal triggered by the Fed’s massive presence in the bond market.” Any efforts to “accurately gauge the pricing distortions these demand dynamics are having” is “impossible. Of course, that assessment comes with it the corollary noted by Ira Jersey (Bloomberg Intelligence chief rates strategist) - If the Fed trims its TIPS buying, it “could be followed by a rise in real yields and a decline in inflation breakevens.”

And it appears that Benjamin Netanyahu's decade-long service as the Prime Minister of Israel may be coming to an end.

As China kicks its vaccination program into high gear.

And it continues to revamp is social legislation including supporting three child households.

While Malaysia implements a 2-week full country lockdown.

Comments

Post a Comment