US Personal Income Apr: -13.1% (est -14.2%; prevR 20.9%; prev 21.1%); US Personal Spending Apr: 0.5% (est 0.5%; prevR 4.7%; prev 4.2%) - details and analysis

- US Personal Income Apr: -13.1% (est -14.2%; prevR 20.9%; prev 21.1%)

- US Personal Spending Apr: 0.5% (est 0.5%; prevR 4.7%; prev 4.2%)

- US Real Personal Spending Apr: -0.1% (est 0.2%; prevR 4.1%; prev 3.6%)

- US PCE Deflator (M/M) Apr: 0.6% (est 0.6%; prevR 0.6%; prev 0.5%)

- US PCE Deflator (Y/Y) Apr: 3.6% (est 3.5%; prevR 2.4%; prev 2.3%)

- US PCE Core Deflator (M/M) Apr: 0.7% (est 0.6%; prev 0.4%)

- US PCE Core Deflator (Y/Y) Apr: 3.1% (est 2.9%; prevR 1.9%; prev 1.8%)

As anticipated, April personal income comes in with a big decline off of March's stimulus infused massive increase, but remains far above pre-pandemic levels. Spending held in with a nominal increase but inflation adjusted it fell a touch m/m. I'll go through each piece independently, but overall a positive report. Tables at the end.

Personal Income

With government transfer payments falling 41% some giveback was inevitable. But looking past that, compensation was up again this month by 0.9% (with wages and salaries up 1%) and proprietor's income built off of last month's very solid 6.2% increase with a gain of 3.1%. So the underlying economy continues to perform well. That's back to back solid improvement for wages, something the Fed has to be eyeing cautiously.

From the report:

The decrease in personal income in April primarily reflected a decrease in government social benefits. Within government social benefits, "other" social benefits decreased as economic impact payments made to individuals from the American Rescue Plan Act of 2021 continued, but at a lower level than in March. Unemployment insurance also decreased, led by decreases in payments from the Pandemic Unemployment Compensation program.

Consumer Spending

As noted, on a nominal basis spending improved over February's huge gains (which were revised up a bit due to a big revision up in durables purchases) but on a real basis (i.e., inflation adjusted) they pulled back a touch. In nominal terms, spending on goods pulled back by 0.6% after being up 9.7% in March with durables up a half percent (was up 14.5% in March) and non-durables falling 1.3% (was up 6.9%). Services purchases were up 1.1% after gaining 2.1% in March.

From the report:

The $80.3 billion increase in current dollar PCE in April reflected an increase of $112.6 billion in spending for services that was partly offset by a $32.3 billion decrease in spending for goods. Within services, the largest contributors to the increase were spending for recreation services and for food services and accommodations. Within goods, a decrease in nondurable goods was partly offset by an increase in durable goods. Within nondurable goods, the decrease was widespread and led by food and beverages. Within durable goods, the increase was accounted for by an increase in motor vehicles and parts.

Personal Savings

Savings rate which had soared to 27.6% in March pulled back to 14.9% in April but this remains well above pre-pandemic levels. I don't have a handy chart, but this is last month's to give you an idea.

Prices

On prices, goods were up 0.7% (same as March) with durables up 1.4% (was 0.6%) and non-durables up three tenths (was eight tenths) m/m. Services were up half percent (same as March which was revised down from eighth tenths). Food was up three tenths and energy fell 0.2% after being up 4.9% in March) m/m. This is the Fed's preferred method for measuring inflation.

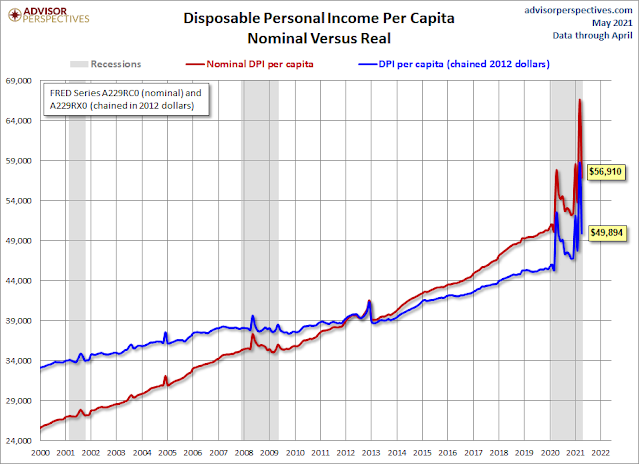

Here's a longer term chart.

Table of m/m income and spending:

Prices

To see more content, including my morning and evening summaries and summaries of some of today's economic reports go to https://sethiassociates.blogspot.com

Comments

Post a Comment