As We Approach The Open... - 9/30/21

As We Approach The Open... - 9/30/21

Please excuse typos. As a side note, after talking with some followers, I'm going to try to make this a little more digestible for those who are not as familiar with the markets, lingo, etc. Feel free to leave your thoughts in the comments section, they are appreciated.

Will start a small glossary at the start also.

As we approach the open of US equity trade in NY, global equities are mixed with US equities looking a lot like this time yesterday (as probably not coincidentally do bond yields) with RUT up just over six tenths, NDX up a half percent and SPX up little over four tenths of a percent.

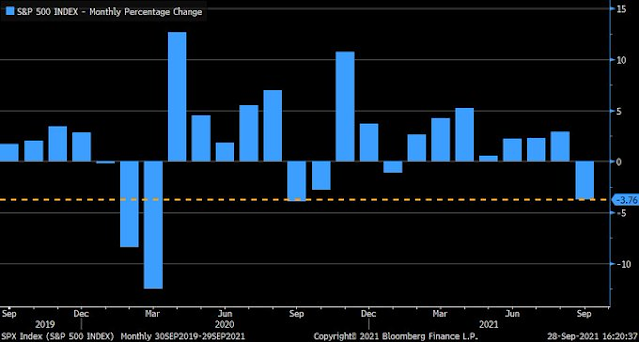

Also of note, today is the last day of the month and quarter.

As the tech correlation with yields has become very negative again.

Major equity indices in the Asia-Pacific region ended Thursday on a mixed note. Japan's Nikkei: -0.3% Hong Kong's Hang Seng: -0.4% China's Shanghai Composite: +0.9% India's Sensex: -0.5% South Korea's Kospi: +0.3% Australia's ASX All Ordinaries: +1.7%. Markets in China will be closed for the next week for Golden Week. I guess the good news is there will probably not be any further negative talking points out of the Chinese leadership. There was more overnight but it's become such a regular occurrence it's hard to keep up with. Also, yesterday, the BOJ bought ETFs for the first time since June on Wednesday. The Topix fell 2%, prompting Kuroda to step in with 70.1 billion yen in stock purchases.

In news, some provinces in China reportedly increased their electricity prices. North Korea indicated that the hotline with South Korea could be restarted in October. BoJ head Kuroda said he saw GDP reaching prepandemic levels next year with 4% growth in 2024.

In economic data China's official Manufacturing PMI fell into contraction for the first time in 18 months while Non-manufacturing PMI returned into expansionary territory in the September reading. Japanese and S Korean industrial production was well under expectations and retail sales missed in both countries as well. All were contractions m/m. Australian construction bounced back.

China's September Manufacturing PMI 49.6 (expected 50.1; last 50.1) and Non-Manufacturing PMI 53.2 (last 47.5). September Caixin Manufacturing PMI 50.0 (expected 49.5; last 49.2)

A little lengthy but here was the commentary:

Commenting on the China General Manufacturing PMI™ data, Dr. Wang Zhe, Senior Economist at Caixin Insight Group said: “The Caixin China General Manufacturing PMI came in at 50 in September, showing that conditions in the manufacturing sector remained unchanged from the previous month. Factors including the reappearance of Covid-19 in several regions and raw material shortages continued to hurt the economy. “Supply in the manufacturing sector continued to shrink, while demand improved. The resurgence of the epidemic in several regions and shortfalls in raw material supplies slowed production at manufacturing companies, with the gauge for output contracting for the second straight month in September. Demand improved, though marginally, with demand for consumer goods in the doldrums. Overseas demand was relatively weak as new export orders largely decreased in September. The epidemic again emerged overseas. Global shipping capacity was also clearly insufficient. “The job market continued to come under pressure. The gauge for employment contracted for the second month in a row in September, and at a faster clip. Manufacturing enterprises reported that they were cautious about hiring new workers. “Inflationary pressure surged. The gauge for input prices hit its highest level in four months in September, its 16th straight month in expansionary territory. The measure for output prices also reached its highest in three months. Surveyed enterprises said the rise in costs was mainly caused by a sharp increase in the prices of energy, industrial metals and electronic raw materials. The pressure of rising costs was partly transmitted downstream to consumers, as the demand was not weak. “In logistics, delivery times grew longer. The gauge of suppliers’ delivery times remained in negative territory due to the lingering effects of some egions’ measures to contain local outbreaks of Covid-19. Consequently, inventories of finished manufacturing goods grew slightly. “Entrepreneurs remained optimistic about the business outlook. The gauge for future output expectations bounced back to the long-term average. Manufacturing enterprises remained positive about the prospects for the market and for getting the Covid-19 outbreak under control. “Overall, conditions in the manufacturing sector picked up in September from the previous month, though the improvement was limited. The Caixin China manufacturing PMI came in at 50, indicating the downward pressure on the economy was still high. On the one hand, the epidemic continued to impact demand, supply, and circulation in the manufacturing sector. The state of the epidemic overseas and the shortage of shipping capacity also dragged down total demand. Epidemic control measures have clearly impacted the logistics industry. “Domestic demand varied based on different types of goods. The demand for intermediate goods and investment goods was relatively high, while the demand for consumer goods was weak, reflecting consumers’ lack of purchasing power. On the other hand, constraints to the supply side were strong as raw material prices remained high and some policy measures restricted production, squeezing employment and eventually weakening demand. “In view of this, in the coming months, the government should focus on improving epidemic prevention and control and alleviating supply-side pressure. It should also find a balance among multiple objectives, such as promoting employment, maintaining the stability of raw material prices, ensuring a stable and orderly supply, and meeting targets for controlling energy consumption."

Japan's August Industrial Production -3.2% m/m (expected -0.5%; last -1.5%), Aug ust Retail Sales -3.2% yr/yr (expected -1.0%; last 2.4%), August Housing Starts 7.5% yr/yr (expected 9.5%; last 9.9%), and August Construction Orders -2.0% yr/yr (last -3.4%)

South Korea's August Industrial Production -0.7% m/m (expected 0.5%; last 0.2%); 9.6% yr/yr (expected 8.2%; last 7.7%). August Retail Sales -0.8% m/m (last -0.6%) and October Manufacturing BSI Index 92 (last 94)

Australia's August Building Approvals 6.8% m/m (expected -5.0%; last -8.6%) and Private House Approvals 3.5% m/m (last -5.5%)

New Zealand's September ANZ Business Confidence -7.2 (last -14.2) and August Building Consents 3.8% m/m (last 2.2%)

Hong Kong's August Retail Sales 11.9% yr/yr (last 2.9%)

As it misses more debt payments.

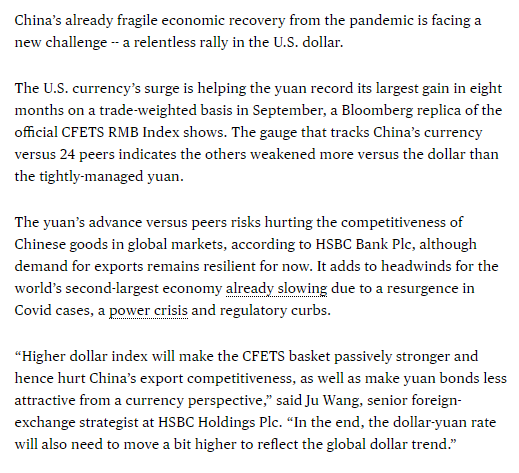

As China has another headwind now in a strong dollar. BBG.

European indices trade in mixed fashion. STOXX Europe 600: +0.3% Germany's DAX: -0.2% U.K.'s FTSE 100: +0.3% France's CAC 40: +0.1% Italy's FTSE MIB: +0.1% Spain's IBEX 35: -0.5%.

In news, the U.K.'s furlough scheme ends today. Bank of England Governor Bailey said that the pace of recovery slowed in recent months and that GDP growth will not return to pre-pandemic levels until next year. Yesterday the British pound fell to the lowest since January as expectations of higher rates were offset by surging energy prices. European Central Bank policymaker Centeno reiterated expectations for inflation to return below 2.0% in 2022. ECB President Lagarde said that the Euro area should be back to pre-crisis GDP late next year. Italy sets a 6% growth target for 2021.

In economic data, EU, Italian and German employment come in close to expectations. UK Q2 GDP was revised up. French consumer spending beat.

Eurozone's August Unemployment Rate 7.5%, as expected (last 7.6%)

Germany's September Unemployment Change -30,000 (expected -33,000; last -53,000) and September Unemployment Rate 5.5% (expected 5.4%; last 5.5%)

U.K.'s Q2 GDP 5.5% qtr/qtr (expected 4.8%; last -1.6%); 23.6% yr/yr (expected 22.2%; last -5.8%). Q2 Business Investment 4.5% qtr/qtr (last 2.4%); UK Private Consumption (Q/Q) Q2 F: 7.2% (est 7.3%; prev 7.3%); UK Gross Fixed Capital Formation (Q/Q) Q2 F: 0.8% (est -0.5%; prev -0.5%) and Q2 Current Account deficit GBP8.60 bln (expected deficit of GBP15.60 bln; last deficit of GBP12.80 bln); UK Nationwide House Prices (M/M) Sep: 0.1% (est 0.6%; prevR 2.0%; prev 2.1%); UK Nationwide House Prices NSA (Y/Y) Sep: 10.0% (est 10.7%; prev 11.0%)

France's August Consumer Spending 1.0% m/m (expected 0.1%; last -2.4%) and August PPI 1.0% m/m (last 1.5%). September CPI -0.2% m/m (expected -0.1%; last 0.6%); 2.1% yr/yr (expected 2.2%; last 1.9%)

Italy's August Unemployment Rate 9.3% (expected 9.2%; last 9.3%). September CPI -0.1% m/m (expected -0.3%; last 0.4%); 2.6% yr/yr (expected 2.4%; last 2.0%)

Spain's July Current Account surplus EUR2.49 bln (last surplus of EUR280 mln) and August Retail Sales -0.9% yr/yr (last -0.1%)

Swiss September KOF Leading Indicators 110.6 (expected 110.0; last 113.5)

And I didn't have time to post yesterday but a little more on the EU confidence numbers.

Economic Sentiment stable in the EU and the euro area, Employment Expectations further up

In September 2021, the Economic Sentiment Indicator (ESI) remained unchanged in the EU (at 116.6) and broadly stable also in the euro area (+0.2 points to 117.8).1 The Employment Expectations Indicator (EEI) increased further (+1.0 point to 113.6 in the EU and +0.8 points to 113.6 in the euro area) reaching its highest level since summer/autumn 2018 in both areas. In the EU, the stability of the ESI in September resulted from improving confidence in construction and among consumers being offset by worsening confidence in services and retail trade. Industry confidence remained unchanged. Amongst the largest EU economies, the ESI rose in Spain (+1.7), Germany (+0.8), the Netherlands and Poland (both +0.6), while it worsened in France (-1.3) and Italy (-0.9).

Commodities/Currencies/Bonds

Bonds - Yields are mixed this morning with 10-year yield up slightly to 1.55% while the 2-year is flat at 0.29%.

Dollar (DXY) - After moving to new 52-week highs (see last night's summary) holding around those levels at $94.36. Daily technicals remain positive but overbought.

VIX - Down a little but remaining over 20 at 21.88.Crude (/CL) - Since failing at $77 WTI on Wednesday has traded weak, down another -1.6% this morning. Currently at $73.66 WTI. Technicals remain positive on daily chart. Coming up on uptrendline.

Natural Gas (/NG) - Bounced off the minor support we noted at around $5.50 up a bit to $5.55.

US Data

Random stuff:

As it appears at least the government shutdown will be averted. Debt ceiling remains an issue of course. BBG.

When gauging supply and demand for shares in the stock market—which determines price—it's important to consider mergers & acquisitions (M&A) since the shares of companies being acquired are removed from circulation. When we account for M&As, the difference between supply of shares and demand for them becomes very lopsided. The chart below shows the 12-month rolling sum.

The chart below shows the cumulative supply and demand since 1982. I view the early 1980s as the start of the modern financial era, so that seems like a good place to start.

On an inflation-adjusted basis, the US equity market cap has grown since 1982 from $1.86 trillion to $38.5 trillion. The supply of equities via IPOs and secondaries totals $5.5 trillion, and the demand for equities from buybacks totals $12.4 trillion. The demand for all equities from M&A totals $26 trillion. The demand from retail investor flows (equity mutual funds, and later on ETFs) is a measly $4.1 trillion, although investor demand is likely much higher than this, since this series does not reflect direct investments or purchases of hybrid funds (e.g. target date). It’s safe to say that the demand for US equities has blown away the supply. Eyeball the chart above: It looks like about a 10-to-1 ratio. We all know that price follows earnings, but in my view the supply/demand dimension is equally important. Every secular trend has its own unique features, and this supply/demand dynamic is a central one for this secular bull. It’s a story that’s fairly unique to the US, which is why the US stock market has dominated the rest of the world.

To see more content, including summaries of most major U.S. economic reports and my morning and nightly updates go to https://seekingalpha.com/user/15085872/instablogs for more recent or https://sethiassociates.blogspot.com for the full history.

Comments

Post a Comment