Daily Summary – February 24, 2021

Daily Summary – February 24, 2021

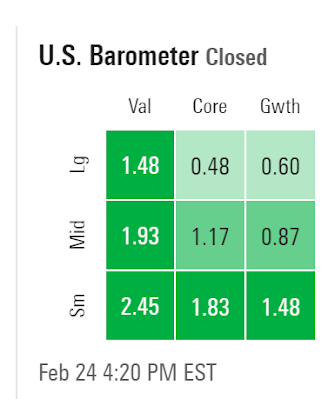

In y'day's conclusion I mentioned y'day had sort of a washout feel and thought we'd likely see a bounce in the SPX and RUT, which we definitely got (RUT was green from the get go), but I wasn't sure about the Naz and NDX given the muted buying volume and technical conditions. But just like y'day (well, actually 20 minutes later today but again right around the time Powell started talking (although we also had a very good new home sales report at that time)) stocks bottomed, and by the end of the day all of the above finished firmly in the green led by RUT up over 2%. SPX was up over 1% and Naz and NDX up just under 1%. The widely watched DJIA also pushed to an ATH today. It was the value stocks which led again, though, and, again, the small value in particular. This recent outperformance has pushed the value/growth ratio to a new 8-mos high and the small value to large growth (IWN/QQQ) to a new recovery high (see charts).

Technically not a lot changed though. SPX and RUT remain in their same channels above their 20-day MA's while NDX and Naz remain beneath both (and Naz has pushed up to just under so that's close resistance now) but above their 50-day MA's. All still have MACD daily sell signals and RSI issues, but with that support, SPX and RUT definitely the safer places to be for now.

With the more positive action SPX sector flag was much improved with nine green sectors led for a third day by energy which was up over 3% for the second day in the last three. Two other sectors up 2% (fins and inds) and three more at least 0.92% (tech, materials, discr). Only one sector down over 1% (utes which went back to a source of funds after a one day pause). Other red sector was staples but was only down fourteen basis points.

In key subsectors, bios finally got a bounce after I called them out y'day but it just took them to the underside of their 50-day so very tenuous for now. Also bouncing back strongly were semi's (which at one point were down 1.5% - they finished up over 3%) and retail although the latter appears to be in part due to more of the call buying of the reddit names (GME, AMC, etc.) so have to discount it again (sigh). Transp another good day pushing further into ATH territory (so another Dow confirmation day (that's for all you old schoolers who know what I'm talking about)).

Breadth told a much better story today where it supported price with 70%+ up volume days for both NYSE (77) and Naz (74). Issues not bad either at 65 and 71 respectively. So for today we can put breadth in the positive column. Hope to see this continue.

Outside of equities, crude, copper, and gold all finished green with crude up to new 52-week high and copper 9-yr high (and it's closing in on that ATH fast). Gold pushed up to the underside of its 20-day MA for a second day but again was rebuffed. The one good thing is that its MACD is ever so close to a close shorts signal which would be an improvement on that indicator. Otherwise its stuck in a downtrend. Really needs this month's low to hold. On the red side were nat gas which sliced right through the 20-day to just above the 100-day. Still remains in an uptrend from the lows in June in the intermediate term though. VIX also red falling right back through all its MA's while long bonds finished down but off the lows with the 10-yr yield falling back under 1.4% after briefly clearing it.

A lot more int'l data points overnight although none that would consider "major" (Japanese LEI's and EU confidence probably closest) followed by jobless claims, durable goods orders, another estimate of 4Q20 GDP, pending home sales, and KC Fed in the US. Also get a huge day for reports with 424(!) with PNGAY, CRM, BUD, DCMYY, ABNB, TD, AMT as our $100B+ market cap companies.

So we got our bounce after a high volume down day. Sometimes that marks the beginning of a run, sometimes it doesn't (I know, hugely helpful). On the side of caution is resistance just overhead for Naz and NDX, some still unresolved technical issues, those yields creeping up that seem to have unnerved some, and what I'd imagine is a monthly rebalancing of some sort needing to be done for those funds that rebalance monthly. But on the other hand, we've got still very liquid conditions, coming stimulus, and vaccines on the side of bulls, and since November those have been a powerful combination.

Comments

Post a Comment